For years, development teams treated qualified charitable distributions (QCDs) like a niche fundraising tool. It was viewed as a helpful option for a tiny fraction of hyper-focused donors, but too complex to anchor a mainstream campaign. That era is officially over. A perfect storm of generational aging and major tax code overhauls has quietly turned direct IRA transfers into one of the most vital revenue engines for modern nonprofits.

The data in our latest 2026 QCD report uncovers a massive disconnect. While the pool of eligible older donors is expanding at a historic rate, actual participation numbers remain low. This creates an “opportunity gap”—a space of unrealized funding that organizations can easily capture by changing how they talk about non-cash assets. Below, we dig into our findings to help your team navigate these changes and maximize funding.

Note: Our findings are based on QCD data from our Smart Giving Suite and survey responses from 230+ nonprofit organizations across a range of different sizes, sectors, and fundraising roles.

Qualified charitable distribution FAQ

If this giving vehicle is new to your nonprofit, explore the following questions before diving into the latest research on the benefits, challenges, and historical impact we’re seeing with QCDs.

What are qualified charitable distributions?

A QCD is a direct, tax-exempt transfer of funds distributed straight from an individual retirement account (IRA) to an eligible 501(c)(3) public charity. This giving vehicle was initially introduced by Congress in the Pension Protection Act of 2006 and eventually made permanent in 2015. Because the funds move directly to the nonprofit without passing through the account holder, the distribution does not count as taxable income for the donor.

What are the rules of QCDs?

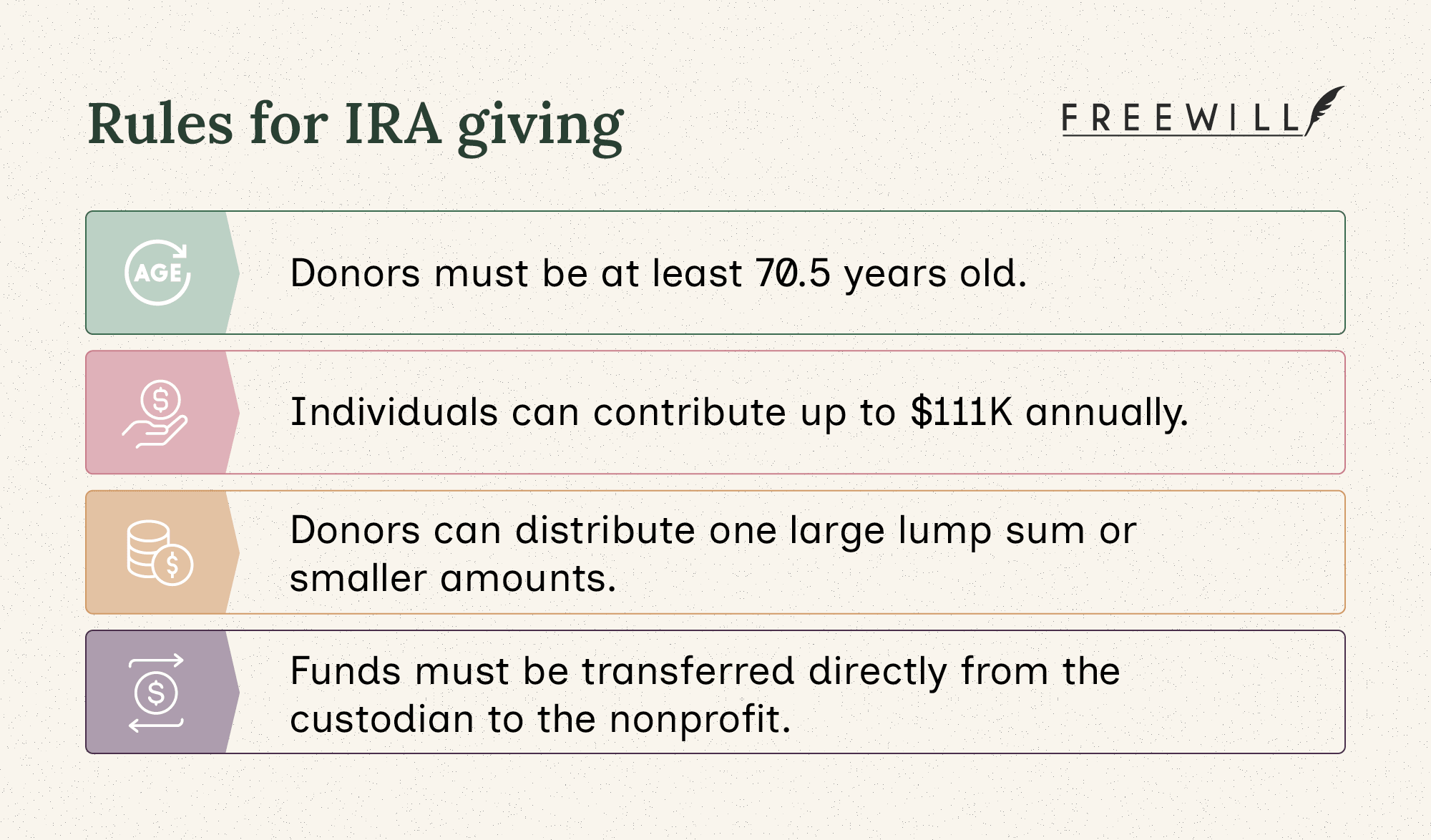

To complete a valid QCD, donors and nonprofits must adhere to a few strict criteria established by the IRS:

- Age threshold: Donors must be at least 70.5 years old at the exact time of the transfer.

- Annual cap: Individual donors can contribute up to $111,000 per year via QCDs. For married couples in which both spouses maintain separate IRAs, each spouse can use the full individual limit, allowing a combined annual limit of up to $222,000.

- Aggregation rule: The annual cap applies to the total sum of all QCDs processed across all of a donor’s IRAs in a single calendar year, meaning they can distribute one large lump sum or break it into smaller amounts over 12 months.

- Distribution mechanics: The money must be transferred directly from the financial institution managing the IRA to the qualified nonprofit. If the check is made out to the donor directly, it loses its tax-free status.

At what age can a donor start making QCDs?

Supporters become eligible the moment they turn 70.5. This creates a highly advantageous strategic window for fundraisers, as required minimum distributions (RMDs) do not legally kick in until age 73. This multi-year gap gives donors a head start to reduce their total balance tax-free before mandatory withdrawals begin.

How do QCDs protect a donor's income from taxes?

Because a QCD acts as an income exclusion rather than an itemized deduction, the gifted amount never factors into a donor’s adjusted gross income (AGI). This omission triggers a highly protective ripple effect across a retiree’s personal finances by preventing Social Security payouts from being pushed into higher tax brackets, keeping Medicare premium surcharges at bay and fully satisfying annual RMD mandates for those 73+.

The exponential growth of QCDs

IRA giving is no longer a quiet alternative for a handful of organizations. It’s an exploding channel for gifts of every size!

According to transaction data from FreeWill’s Smart Giving Suite, completed QCD gifts jumped by 56% in 2024, followed by another 47% increase over the course of 2025. Looking at the broader timeline, the cumulative value of these direct transfers has grown by more than 390% since 2019.

This momentum is not restricted to ultra-wealthy individuals. When we look at transaction volume since 2019 grouped by gift size, the shifts are astounding:

- Gifts under $1K have risen by 840%.

- Gifts between $1K and $5K have climbed by 975%.

- Major gifts exceeding $10K have skyrocketed by 1,290%.

With an overall average gift size of $4K in 2025, supporters are demonstrating that they prefer giving from their financial accounts over traditional paper checks, cash, and credit card donations.

The 2026 tax landscape: Why cash is losing to QCDs

The rollout of the One, Big, Beautiful Bill (OBBB) fundamentally changed the financial playbook for retirement giving. Though the legislation preserved the core structure of the QCD itself, it erected steep new tax walls around standard cash contributions starting in 2026.

Under these new rules, older donors who write standard checks or make credit card donations face major limitations on their tax advantages, such as:

- The 0.5% AGI deduction floor: Taxpayers who itemize can only deduct charitable gifts that surpass 0.5% of their AGI. So, for an individual making $100,000, their first $500 in standard donations yields zero tax benefits.

- The benefit limit for high earners: High-earning taxpayers in the top 37% bracket have hit a new ceiling. The OBBB restricts the maximum tax benefit of their itemized write-offs to 35%, eroding the financial incentive of a cash gift compared to previous tax years.

The structural advantage of direct transfers

A QCD sidesteps both of these issues, because it acts as a direct exclusion from the donor's gross income rather than an itemized deduction. Because the money never counts as taxable income, it lowers their tax bill from the very first dollar. This protects high earners and shields everyday retirees from hitting the AGI floor.

When you factor in the OBBB’s temporary Senior Tax Deduction through 2028—which inflates the standard deduction even further—itemizing simply doesn't make sense for most retirees. Consequently, an IRA transfer is the most effective way for seniors to support a cause without taking a heavy tax hit.

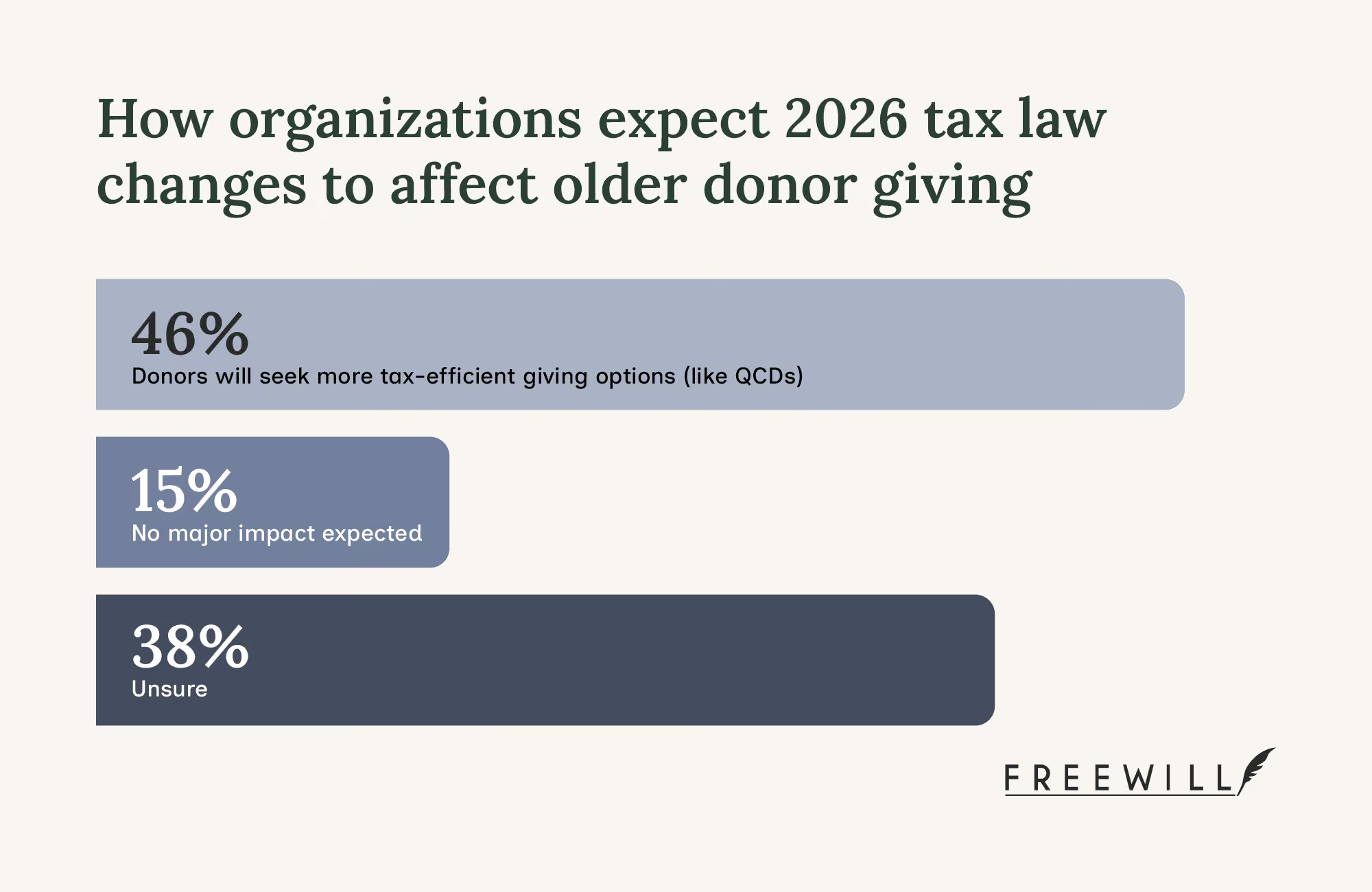

The fundraising sector is preparing for this shift: 46% of surveyed organizations predict that older supporters will actively seek out tax-advantaged giving vehicles like QCDs to sustain their philanthropy.

Top 3 operational obstacles for QCD fundraising

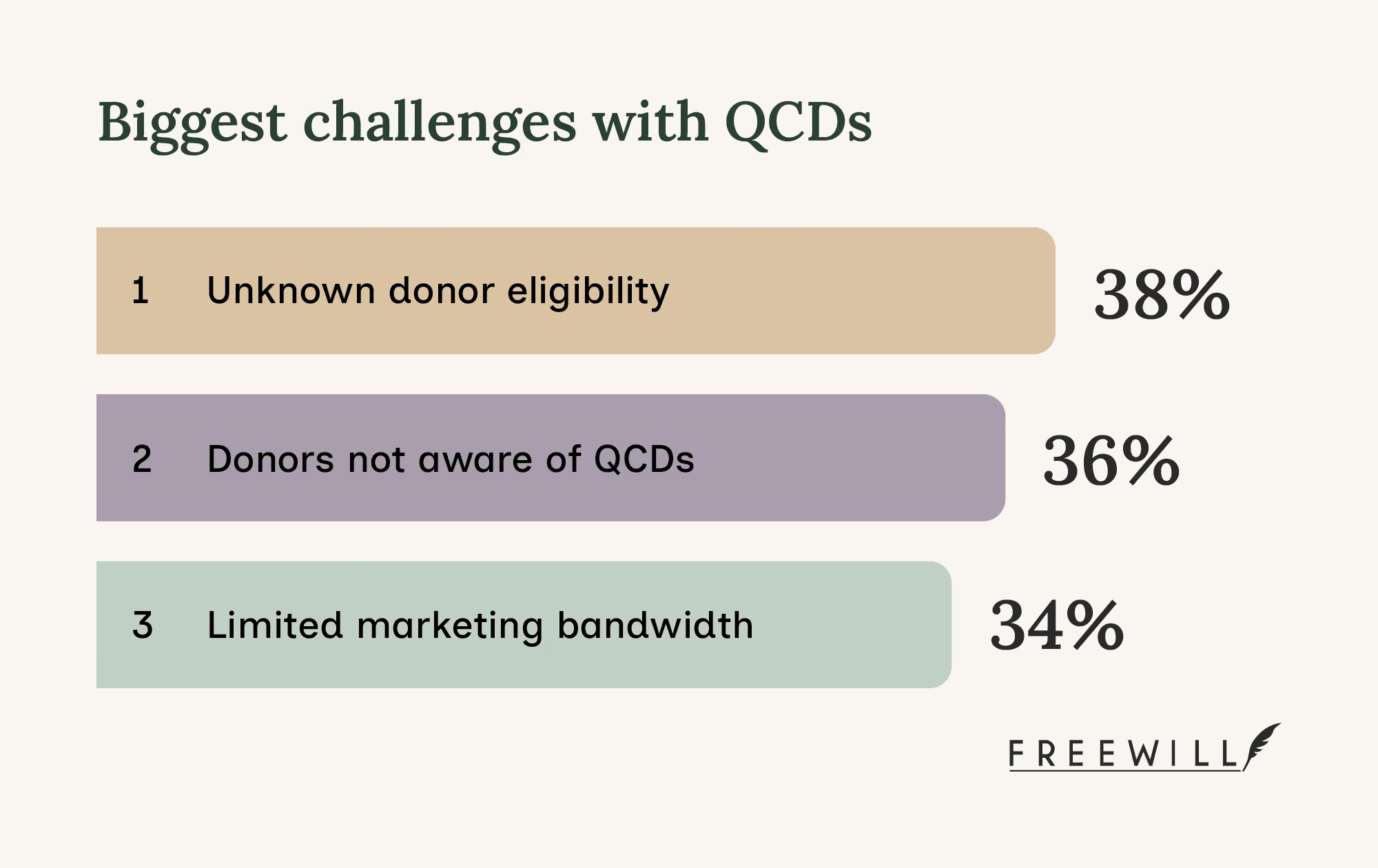

Even with the undeniable financial benefits for donors, many internal fundraising teams are leaving money on the table due to operational bottlenecks. When we asked nonprofit staff to name the biggest friction points stalling their QCD giving programs, three distinct challenges emerged:

- Identifying who is actually qualified (38%): This problem is further exacerbated by internal tracking habits, as 31% of nonprofits don’t record donor age data in their systems.

- Low donor awareness of QCDs (36%): Many eligible supporters remain in the dark about how these accounts function or why a direct transfer is better than cash.

- Strained marketing resources (34%): Stretched fundraising departments often lack the time, software, or baseline bandwidth to build dedicated QCD outreach.

Quantifying the opportunity gap

The challenges we covered above explain the current opportunity gap that nonprofits are experiencing. There’s a stark divide between the volume of age-eligible donors and the tiny fraction who actually utilize the vehicle.

Right now, the sector is experiencing “Peak 65,” a historic surge as more Americans turn 65 than ever before. Nonprofits are feeling this shift directly: one-third of surveyed organizations (33%) report that more than 50% of their entire donor base has passed the 70.5 age threshold.

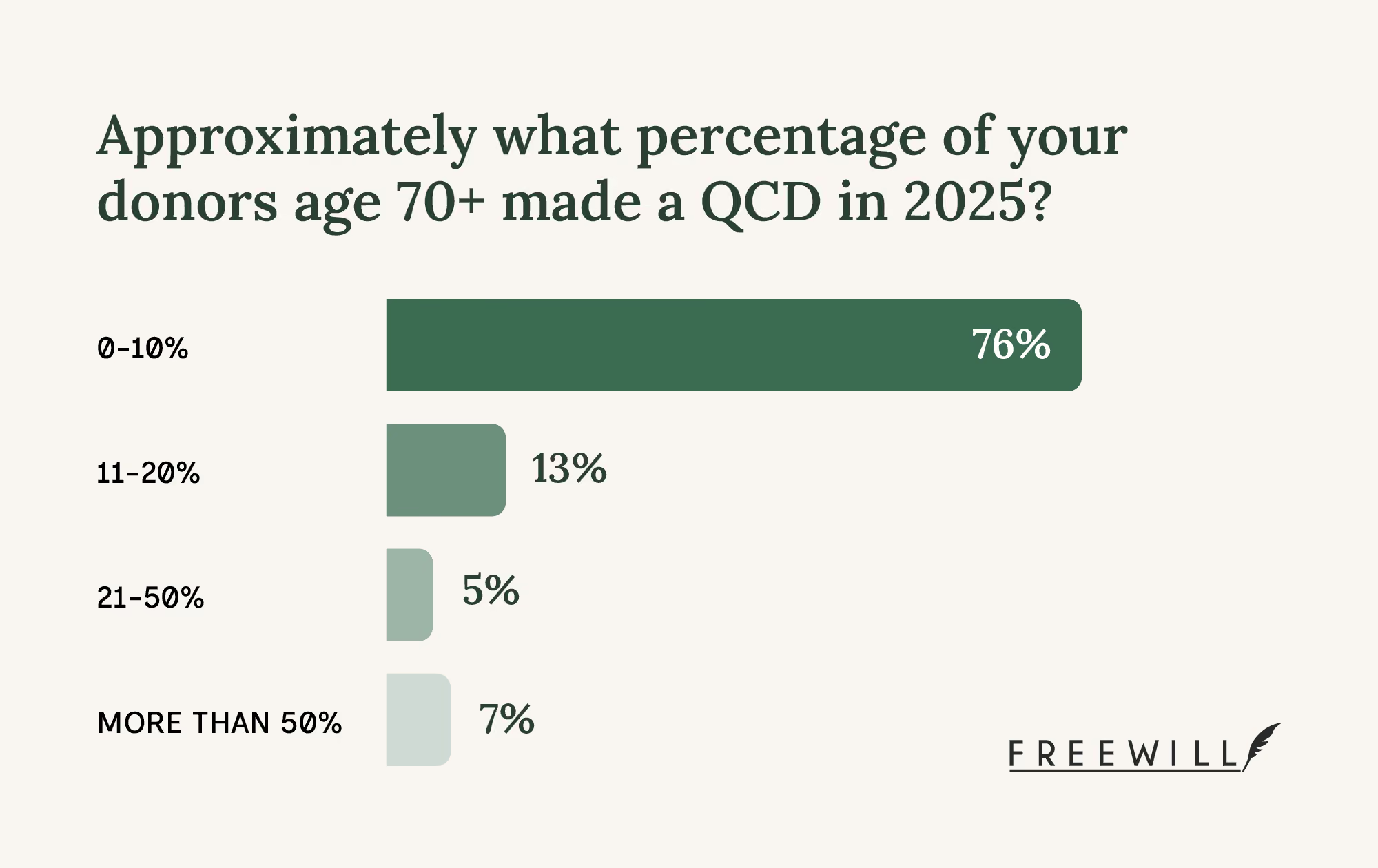

Yet, despite having an audience full of eligible supporters, actual utilization is remarkably stagnant. A striking 76% of organizations say that fewer than 10% of their eligible mature donors made a QCD in 2025.

The data proves that an aging donor list doesn’t automatically generate non-cash revenue. Even at nonprofits where more than half of the donor list is old enough to qualify, participation rates rarely exceed 10%.

Demographics alone aren’t enough! Intentional education is the missing link.

QCD marketing strategies that drive results

Our QCD report uncovered a direct link between proactive outreach, staff confidence, and actual fundraising returns. Organizations that intentionally promote QCDs see completely different outcomes than those that treat it as an afterthought.

Here are a few key takeaways from our report:

- Regular promotion matters. Nonprofits that promoted QCDs at least four times throughout the year were more likely to raise $100K or more through that vehicle, so work non-cash giving into your marketing plan!

- Timing makes a difference. Nearly 7 in 10 organizations report that QCD gifts peak at the end of the year, likely driven by factors like RMD deadlines and year-end appeals.

- Confidence in outreach boosts results. Confidence builds donor trust! Every organization that felt “extremely confident” raised over $100K in QCDs in 2025. Meanwhile, 81% of organizations that didn’t feel confident at all raised less than $10K.

Scaling your revenue with FreeWill

To simplify IRA giving, turn to specialized technology like FreeWill. Our Smart Giving Suite empowers teams to collect powerful, tax-advantaged gifts like QCDs, DAFs, stocks, and crypto.

Seamlessly scale your fundraising program by tapping into these benefits:

- Year-round marketing support: Maximize your revenue potential beyond the year-end rush with intuitive tools that maintain consistent, automated multi-touchpoint communications.

- Frictionless donation experience: Make it incredibly easy for age-eligible supporters to navigate the QCD giving process and successfully initiate direct IRA transfers.

- Performance tracking and gift alerts: Gain full visibility into QCD performance. You’ll receive updates and donor information as gifts are completed.

Don’t just take our word for it. Hear how NOCO Humane used FreeWill to educate their donors and raise more through non-cash gifts:

Start modernizing your giving options and diversifying your revenue streams. Accepting QCDs is easier than you think with FreeWill.

Wrapping up

Our report uncovers a promising truth: you do not have a generosity problem. Your older supporters are ready and willing to give QCDs. They simply don’t know they qualify, are confused by the execution steps, or don’t realize your organization is set up to receive direct IRA transfers.

Fixing this disconnect simply requires a smart pivot in how you educate the loyal givers already sitting in your database.

The industry is moving quickly. 96% of organizations plan to increase their QCD marketing efforts. Don’t get left behind! Join them by using a solution like our Smart Giving Suite to bypass limited marketing bandwidth, educate donors, and unlock high-value revenue!

Continue exploring the power of tax-advantage giving with these resources:

- Planned giving: A nonprofit's guide to growing legacy gifts

- How to accept crypto donations: Complete nonprofit guide

- How to accept stock donations: Easy steps for nonprofits